From Our Two Cents Monthly Newsletter – September 2017 Edition.

Personal finance ratios

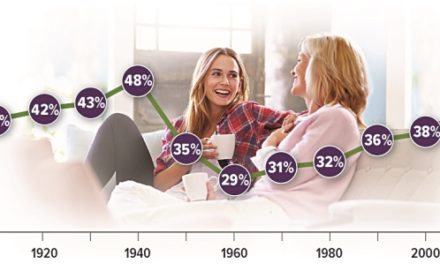

Personal savings

Personal savings

Debt-to-income

Debt-to-income

As its name would indicate, a debt-to-income (DTI) ratio is the proportion of an individual’s monthly debt payments in relation to his or her gross monthly income. Many lenders use DTI a s a primary indicator of worthiness of loans because it gauges the individual’s ability to cover loan payments. Though there is no consistent, unilateral recommended ratio, it is popular convention that a DTI over 40 percent will make it more difficult to secure a loan.

Liquidity

Liquidity

This ratio is used to determine how an individual is able to make ends meet in the event of an emergency. Liquidity is calculated by taking all liquid assets (such as nonqualified accounts and cash) divided by fixed monthly expenses (like debt payments ). It is commonly suggested that an individual should have 3-6 months ’ worth of expenses in liquid assets.

Debt-to-asset

Debt-to-asset

The debt-to-asset ratio is calculated by taking an individual’s total debt divided by their total assets. Though this ratio is primarily used in relation to a company’s finances, it is used to help lenders understand an individual’s borrowing habits, specifically how much of their net worth is tied up in hard assets.

{kind=link}