How to Correct an Error on Your Credit Report

According to the Consumer Financial Protection Bureau (CFPB), credit report errors more than...

Read More

According to the Consumer Financial Protection Bureau (CFPB), credit report errors more than...

Read More

Are You a HENRY? Consider These Wealth-Building Strategies HENRY is a catchy acronym for...

Read More

Buying a home is a long-term commitment, so it’s not surprising that older Americans are...

Read More

After pushing interest rates gradually upward for three years, the Federal Reserve dropped the...

Read More

Term life insurance provides life insurance coverage for a specific time period (the term). The...

Read More

In early 2020, 61% of U.S. workers surveyed said that retirement planning makes them feel...

Read More

Here are some things to consider as you weigh potential tax moves before the end of the year....

Read More

Federal and state governments have spent extraordinary sums in response to the economic toll...

Read More

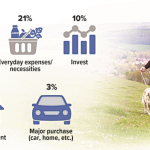

Whether checking out at your local supermarket, filling up with gas at the corner station, or...

Read More

With winter just around the corner and freezing temperatures arriving early in many states, some...

Read More

Moving can be a stressful experience in many ways. Not only do you need to prepare nearly...

Read More

Changing jobs is one of the biggest life decisions you can make and doing so presents an important...

Read More